Insider Transactions: The Basics

"There's no better indicator of a company's future than the people running it putting their own money into the stock." — Joel Greenblatt

In spring 2025, two insiders at Signet Jewelers (NYSE: SIG) independently purchased stock on the open market. On March 31, CEO J.K. Symancyk committed $861,750 of personal capital in a single transaction, acquiring 15,000 shares near $57 per share. A few weeks later on April 25, independent director Helen McCluskey added another $100,062 of her own money.

No option exercise, no stock grant — personal checks. The combined cluster purchase totaled roughly $962,000 in discretionary buying, concentrated in a four-week window while the stock traded below $60.

By April 2026, the stock had risen to roughly $93, a +63% return, with a peak above $106 along the way (a +86% peak return). The transactions were disclosed in two ordinary Form 4 filings on SEC EDGAR, visible to anyone who knew where to look. Tradetheon's signal detection would flag this pattern as a Cluster Buy paired with a C-Suite Purchase — two of the highest-conviction insider signals available in public data.

Who counts as an "insider"?

When people hear "insider trading," they usually think of something illegal. But most insider trading is perfectly legal — and publicly reported.

SEC rules define an insider as any officer (CEO, CFO, COO, etc.), director, or beneficial owner holding more than 10% of a company's equity. When these people buy or sell their company's stock on the open market, they must file Form 4 with the SEC within two business days.

This is a different kind of signal from 13F data. A 13F tells you what an outside investor with deep research capabilities believes. A Form 4 tells you what someone inside the company is doing with their own money.

Going deeper

The SEC requires three types of insider filings: Form 3 (initial statement of ownership, filed when someone becomes an insider), Form 4 (changes in ownership, filed within 2 business days of a transaction), and Form 5 (annual summary of transactions that could have been reported on Form 4). Tradetheon ingests all three from SEC EDGAR daily.

Why insider purchases matter more than sales

This is the single most important concept in insider transaction analysis.

Purchases are almost always informative. When a CFO writes a personal check for $200,000 of company stock, they already have concentrated exposure through salary, bonus, and unvested equity. They're voluntarily adding more. There is essentially one reason: they believe the stock is undervalued relative to what they know about the business.

Sales are usually noise. Executives sell for estate planning, to pay taxes on exercised options, to purchase a new home, to fund another business, or through pre-scheduled plans that execute automatically. A single executive selling 5% of their holdings is almost never a meaningful signal.

Academic research confirms this asymmetry decisively. Lakonishok and Lee (2001) studied the full universe of insider transactions and found that stocks with heavy insider purchasing outperformed the market by 4.8% over the following 12 months (after controlling for size and book-to-market factors). Insider selling had almost no predictive value.[1] Jeng, Metrick, and Zeckhauser (2003) estimated insider purchase portfolios earned abnormal returns of roughly 6% annually.[2]

Going deeper

Jeng, Metrick, and Zeckhauser found that insider purchase portfolios earn abnormal returns of about 40 basis points per month. Of those returns, roughly one-sixth accrues within the first five days and about one-third within the first month after the trade.[2] This suggests that while insiders do have timing ability, the bulk of the signal plays out over quarters and years, not days. Following insider purchases requires the same patience the insiders themselves need.

Not all sales are noise: skin-in-the-game erosion

While routine insider selling is noise, framing all sales as useless disregards the first principle of indirect information: what insiders do with their own money matters. Sales that meaningfully reduce an insider's skin in the game deserve attention, even if they carry less signal than purchases.

Tradetheon therefore generates two sale-side signals, calibrated at higher thresholds than the purchase-side equivalents to filter out routine liquidation:

Significant Sell — A discretionary sale large enough in dollar terms or as a percentage of the insider's holdings that it meaningfully erodes their personal stake. A CEO liquidating 40% of their vested shares into an open market — not through a 10b5-1 plan, not coincident with an option exercise — tells you something about how they view the stock's forward risk-reward.

Cluster Sell — Multiple insiders selling within 30 days under discretionary circumstances. Just as clustered buying reflects shared conviction, clustered selling can reflect shared concern. The threshold is set higher than for Cluster Buy because sale clustering is more often driven by common tax or liquidity events (year-end planning, IPO lockup expirations, coordinated 10b5-1 plan rollouts).

These signals don't replace purchase-side analytics — purchases remain the dominant signal because the motivation space is narrower. But a CEO who sells aggressively and repeatedly while publicly expressing confidence in the business creates a tension between words and actions that's worth understanding.

What is a 10b5-1 plan?

You'll encounter this term frequently. A 10b5-1 plan is a pre-arranged trading schedule that allows insiders to buy or sell shares at predetermined times and quantities, established when they are not in possession of material non-public information.

The purpose is to give insiders a legal safe harbor: by committing to a trading plan in advance, they can sell stock without being accused of trading on inside knowledge. Once the plan is in place, trades execute automatically on schedule regardless of the company's current situation.

In practice, this means a large portion of insider sales in Form 4 filings are plan-driven — the CEO didn't decide to sell yesterday because they know bad news is coming; they set up this schedule months ago.

Going deeper

10b5-1 plans have faced scrutiny. The SEC introduced new rules in 2022 requiring a 90-day cooling-off period between establishing or modifying a plan and the first trade executing under it. Insiders must also certify they are unaware of material non-public information when adopting the plan. These reforms were prompted by concerns that some executives were timing plan adoption or modification to exploit informational advantages. No peer-reviewed research has conclusively established whether 10b5-1 plans are systematically gamed, but the regulatory concern was significant enough to produce the 2022 amendments. For Tradetheon's purposes, we focus on open-market, discretionary transactions — both purchases and the sale-side signals above exclude plan-driven activity wherever Form 4 disclosure allows us to identify it.

Tradetheon's Insider Record page offers two filter checkboxes — EXCL ROUTINE and EXCL 10B5-1 — that let you exclude plan-driven and routine transactions from the data view. This helps you focus on discretionary open-market activity, where the signal-to-noise ratio is highest.

Tradetheon's insider signals

Tradetheon detects five types of insider signals. We limit the signal detection window to the trailing 2 years of transactions — signals older than that are untimely even for long-term investors. The full history available on Tradetheon covers the most recent 5 years, which is more than sufficient to establish behavioral baselines for nearly every active insider.

Cluster Buy — the strongest signal

Two or more insiders purchasing within 30 days of each other. When the CEO and a board member independently write personal checks for nearly $1 million of company stock in the same month — as happened at Signet Jewelers in spring 2025 — they're reaching the same conclusion about valuation based on deep company knowledge.

Alldredge and Blank (2019) studied insider clustering directly and found that clustered purchases earned abnormal returns of approximately 3.8% over 21 trading days — nearly double the 2% return for non-clustered purchases.[3]

C-Suite Purchase — seniority matters

A purchase by the CEO, CFO, or other senior officer. These executives have the broadest operational visibility — financial performance, competitive dynamics, upcoming developments.

Knewtson and Nofsinger (2014) found that CFO purchase portfolios were among the most profitable of all insider roles. Their explanation: CFOs face somewhat less regulatory scrutiny than CEOs, which may allow them to trade more freely on their operational knowledge. Post-SOX reforms narrowed this gap, but CFO purchases remain a high-conviction signal.[4]

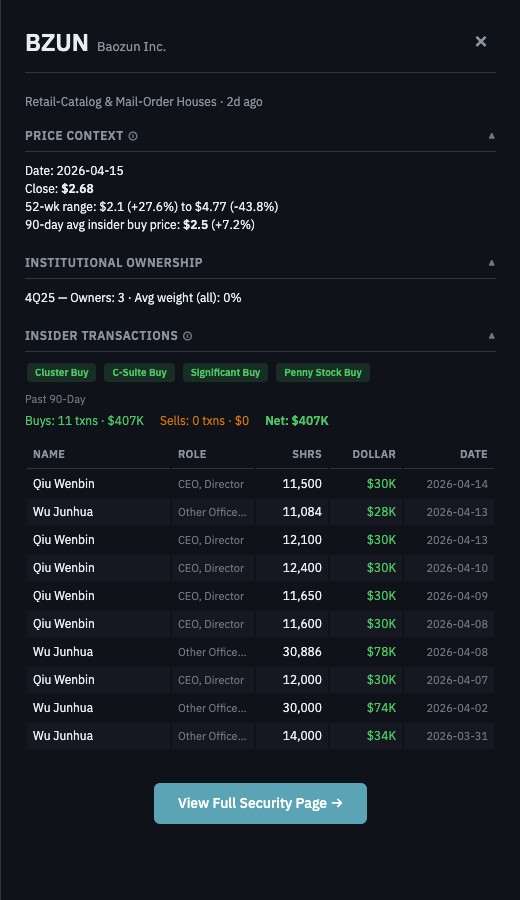

Here is an example from BZUN (Baozun Inc.), where the CEO and another officer accumulated shares over several weeks — triggering Cluster Buy, C-Suite Buy, and Significant Buy signals simultaneously:

Significant Buy — magnitude matters

A transaction exceeding $100,000 or representing more than 20% of the insider's existing position. A $25,000 purchase from an executive earning $5 million per year is a rounding error. The Signet CEO's $862K single-transaction purchase is a meaningful commitment of personal capital that's hard to explain away as incidental.

Significant Sell and Cluster Sell — skin-in-the-game erosion

See the section above. These are surfaced at higher thresholds than the purchase-side signals and are intended as a complement to, not a substitute for, the buy-side analysis.

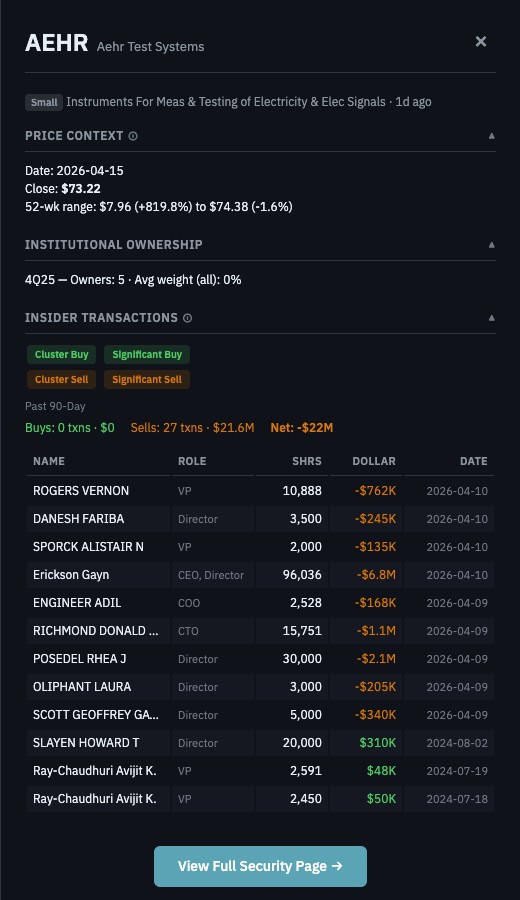

Here is an example from AEHR (Aehr Test Systems), where multiple insiders sold within a short window — triggering Cluster Buy, Significant Buy, Cluster Sell, and Significant Sell signals. The drawer shows the full transaction history and the net dollar flow:

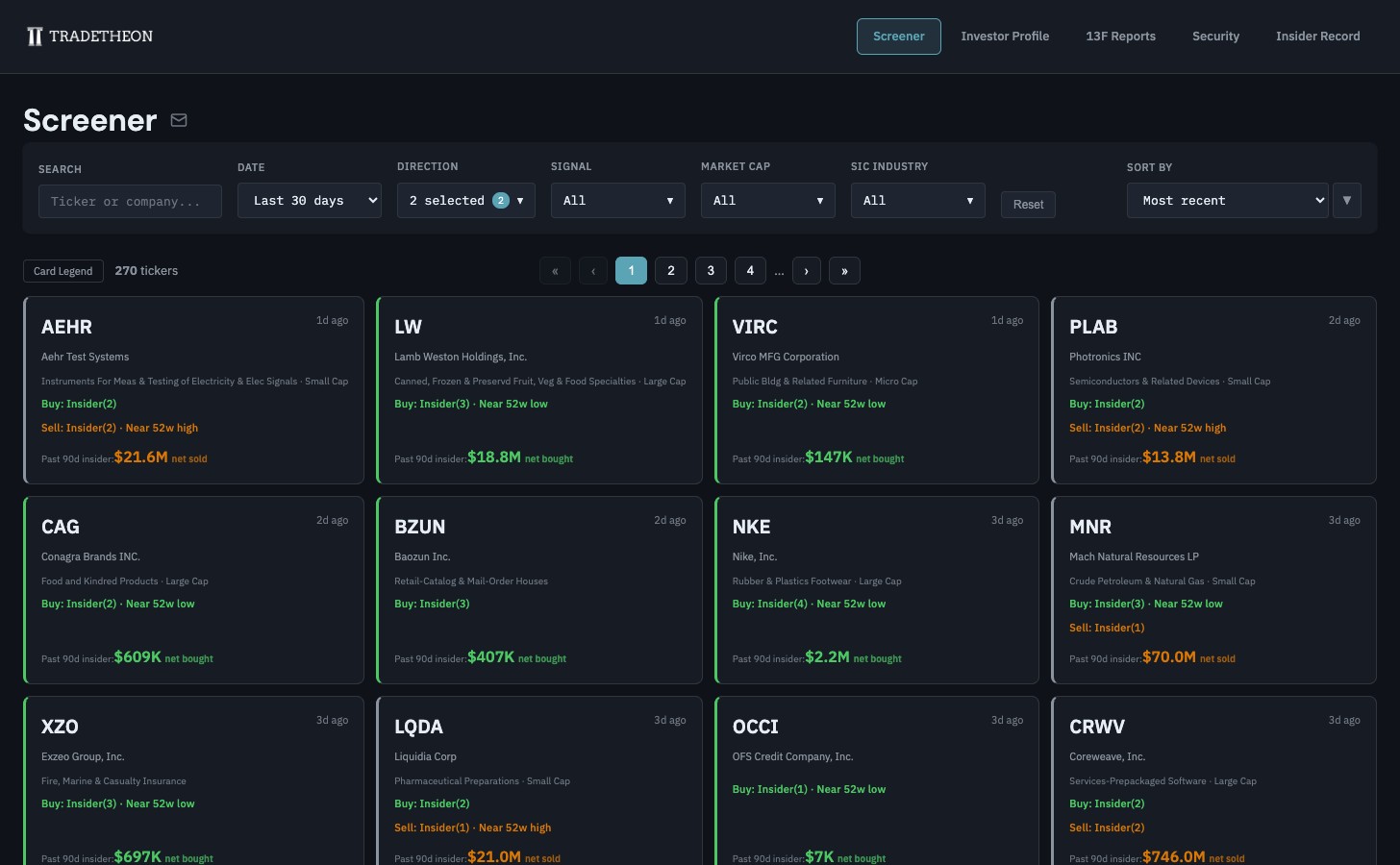

The Screener surfaces these signals as ticker cards, each showing which signals fired, the insider transaction direction, and the net dollar amount over the past 90 days. You can filter by signal type, direction, market cap, and industry to focus on the patterns that match your investment style.

Filtering out routine trades

Not every Form 4 filing is worth your attention. Tradetheon filters the raw data to surface the transactions that research and practice suggest carry predictive value:

Open-market, discretionary transactions only. We separate discretionary open-market activity from option exercises, stock grants, gifts, and pre-scheduled 10b5-1 trades wherever the filing discloses enough to identify the difference. An option exercise followed by an immediate sale is a liquidity event, not a conviction signal.

Minimum thresholds. Small insider purchases — a director buying $5,000 of stock as a token gesture after joining the board — are included in the raw data but don't trigger signals. Thresholds were calibrated to flag transactions that represent genuine financial commitment.

Purchase-weighted signal generation. Purchase-side signals fire at lower thresholds than sale-side signals, reflecting the academic asymmetry in signal-to-noise ratio.

Caveats you need to understand

-

Insiders are often early. This is the number-one reason people get frustrated following insider data. An insider who buys at $50 might watch the stock drop to $35 before it eventually reaches $80. The academic evidence shows insider purchases are predictive over 6–12 month horizons, not days or weeks. Following insider buys requires the same patience the insiders themselves need. If you're looking for a short-term trading signal, insider data is the wrong tool.

-

Penny stocks and micro-caps are noisier. Insider signals in very small stocks carry additional risk. Low-liquidity, low-priced stocks are more susceptible to market manipulation, and the population of insiders at micro-cap companies is less scrutinized by regulators and analysts. An insider purchase at a $50 million market cap company may reflect genuine conviction — or it may be part of a promotional scheme. Tradetheon does not exclude small-cap insider transactions, but users should apply extra skepticism to signals from companies with very low market capitalization or share prices. The cluster buy and significant buy thresholds help filter here: manipulation typically involves isolated actors, not clusters of independent insiders each spending six figures.

-

A Form 4 tells you what happened, not why. An insider buying after a guidance cut might be seeing long-term value the market is missing — or might be throwing good money after bad. The transaction is a prompt for your own research, never a conclusion.

-

Dataset boundaries. Tradetheon displays up to 5 years of insider transaction history per insider (our underlying data goes back further, but 5 years is what surfaces in the UI). For most insiders, this is more than sufficient to establish behavioral baselines — how frequently they buy, at what sizes, and whether their past purchases were well-timed. For executives who were active before the displayed window, we can't distinguish a genuinely rare buyer from someone whose early activity simply isn't shown. Since signal detection focuses on the most recent 2 years of activity, this left-edge limitation affects historical context more than current screening.

💡 Tip: Context isn't in the filing — read the transcripts

A Form 4 tells you what, not why. One of the most effective ways to fill this context gap is to read earnings call transcripts alongside the insider data. Management teams are legally constrained in what they can promise publicly, but what they choose to emphasize — and what they avoid discussing — helps you read between the lines. When a CFO buys $300,000 of stock two weeks after a call where management guided capex meaningfully higher, the filing and the transcript together tell a richer story than either alone: management is publicly willing to spend more today because they expect the payoff, and the CFO is personally backing that view with their own money. What they did helps you interpret what they said.

A note on expectations

Every strategy weakens when it becomes crowded. The academic studies cited throughout this guide are empirical and replicable, but they measure alpha over historical time windows — often decades ago, in market environments that no longer exist. Evidence that a signal worked from 1976 to 2006, or that a cluster buy paid off in 2025, is not a guarantee the same pattern will work going forward. Overreliance on any signal — including the ones Tradetheon surfaces — to make concentrated investment decisions is not prudent. Use this data as one input into your own fundamental analysis, not as a substitute for it.

Start exploring by checking the insider and institutional signals in the Screener tab or finding your favorite manager at Investor Profile.

Sources

[1] Lakonishok, J. & Lee, I. (2001). "Are Insider Trades Informative?" Review of Financial Studies, 14(1), 79–111. → Paper

[2] Jeng, L., Metrick, A., & Zeckhauser, R. (2003). "Estimating the Returns to Insider Trading: A Performance-Evaluation Perspective." Review of Economics and Statistics, 85(2), 453–471. → Paper

[3] Alldredge, D. & Blank, B. (2019). "Do Insiders Cluster Trades With Colleagues? Evidence From Daily Insider Trading." Journal of Financial Research, 42(2), 331–360. → Paper

[4] Knewtson, H. & Nofsinger, J. (2014). "Why Are CFO Insider Trades More Informative?" Managerial Finance, 40(2), 157–175. → Paper